The cost of providing a Christmas party is income tax deductible to the extent that it is subject to FBT. Therefore, any costs that are exempt from FBT cannot be claimed as an income tax deduction. GST credits can only be claimed to the extent that a cost is tax deductible. Therefore, if you cannot claim it as a deduction, you cannot claim the GST credits either.

The ATO have guidelines in regards to FBT as it relates to different business structures. Go to www.ato.gov.au for more information.

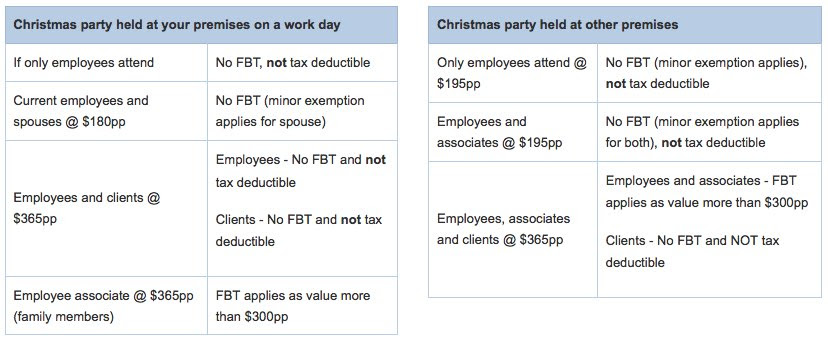

What can you Claim

Minor Benefits Exemption

The $300 threshold is applied separately to each benefit, gift or party. So for example, an employee could attend the workplace party at a cost to the employer of $280 and receive a gift worth $250, but because these amounts are treated separately there are no FBT implications.

The minor benefit exemption does NOT apply to any party other than employees. Therefore if a non-entertainment gift is given to a client or supplier this can be deductible expense and therefore GST can be claimed.

Christmas Gifts for your Employees

Are gifts to your employee claimable? Gifts may be classified as “entertainment” or “non-entertainment”.

The provision of a gift to an employee at Christmas time, such as a hamper, may be a minor benefit that is an exempt benefit where the value is less than $300. Where the gift is given at the Christmas party, each benefit can be considered separately.

1. For gifts such as wine, food, hampers, vouchers, etc., these are not considered to be entertainment.

- If the gift is a minor benefit (i.e., less than $300 value), then the gift is tax deductible, and therefore GST is claimable for gifts to employees and their family members, clients and suppliers. No FBT applies to gifts of less than $300.

- For gifts over $300, FBT may apply for employees and their family members.

2. Gifts such as a holiday, membership to a club, or tickets to a theatre, sporting or musical event are considered to be entertainment.

- For minor benefits, as above, the gift is not tax deductible and no FBT applies.

- For employees this is not a minor benefit, the gift is tax deductible but it is also subject to FBT.

Christmas Gifts for your Clients and Suppliers

Are gifts to your clients and suppliers claimable? Gifts may be classified as “entertainment” or “non-entertainment”.

1. For gifts such as wine, food, hampers, vouchers, etc., these are not considered to be entertainment.

- Non-entertainment gifts to clients or suppliers are deductible and GST is claimable.

2. Gifts such as a holiday, membership to a club, or tickets to a theatre, sporting or musical event are considered to be entertainment.

- For clients and suppliers, the entertainment gift is NOT tax deductible, and no FBT applies, no GST is claimable.

Giving your clients a gift at Christmas is a personal choice that you as the business owner can make. Be aware that some clients may not be allowed to accept gifts due to their business’s Code of Conduct (e.g., government workers).

DISCLAIMER: Great Perth Bookkeeping is not authorised to provide tax advice. We remind you that the topic of entertainment, tax deduction and fringe benefits tax is complex and not always straightforward. Check with your tax agent if in doubt and refer to the ATO website for detailed guidance.